Tata Capital Ltd IPO — In-Depth Report & Market Update

1. Company at a Glance

Tata Capital Limited (TCL), the flagship financial services arm of the Tata Group, stands as one of India’s leading diversified non-banking financial companies (NBFCs). It offers a full spectrum of products — from consumer and SME finance to corporate lending, infrastructure funding, wealth management, and investment banking.

The company’s upcoming public issue represents a significant regulatory and strategic milestone, as the Reserve Bank of India (RBI) has mandated the listing of large “upper-layer” NBFCs. Tata Capital’s IPO is both a compliance step and an opportunity to strengthen its balance sheet, brand visibility, and retail investor participation.

2. Latest Market Updates (as of October 2025)

3. IPO Structure & Key Terms

| Parameter | Details |

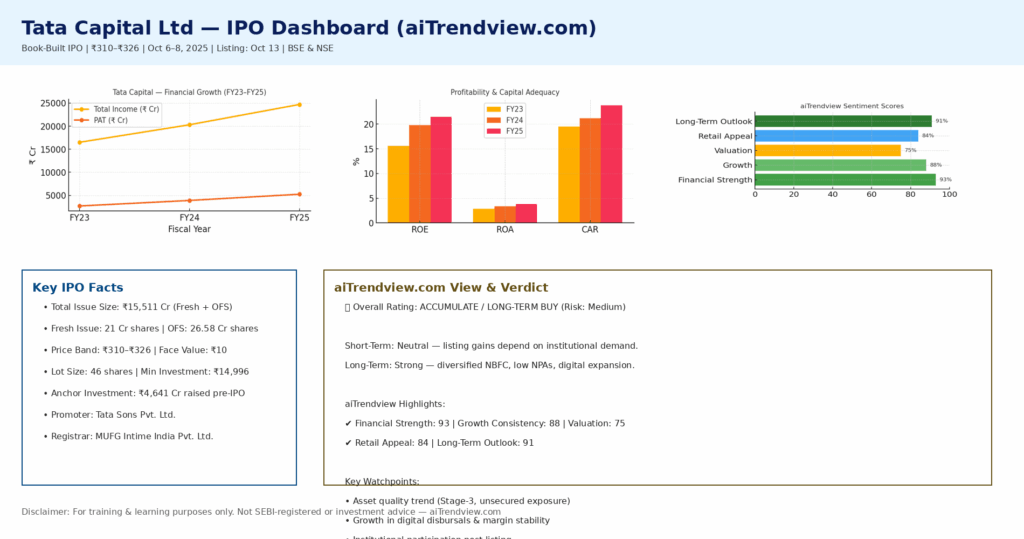

| Total Issue Size | ~₹15,511 crore |

| Fresh Issue | Up to 21 crore equity shares |

| Offer for Sale (OFS) | Up to 26.58 crore shares (Tata Sons, IFC, and others) |

| Face Value | ₹10 per share |

| Price Band | ₹310 – ₹326 per share |

| Lot Size | 46 shares (min investment ₹14,996) |

| Anchor Bidding | October 3, 2025 |

| Public Bidding | October 6 – 8, 2025 |

| Allotment | October 9, 2025 |

| Refunds / Demat Credit | October 10, 2025 |

| Listing Date | October 13, 2025 |

| Promoter | Tata Sons Pvt. Ltd. |

| Post IPO Promoter Holding | Likely to dilute from 95.8% |

| Registrar | MUFG Intime India Pvt. Ltd. |

4. Financial & Operational Highlights

| Metric | FY23 | FY24 | FY25 |

| Total Income (₹ Cr) | 16,500 | 20,300 | 24,700 |

| Profit After Tax (₹ Cr) | 2,700 | 3,900 | 5,250 |

| ROE (%) | 15.6 | 19.8 | 21.5 |

| Gross NPA (%) | 2.03 | 1.82 | 1.57 |

| Net NPA (%) | 0.57 | 0.46 | 0.39 |

| Capital Adequacy Ratio (%) | 19.5 | 21.2 | 23.8 |

✅ Strong financial trajectory: 3-year CAGR of ~21% in revenue and ~40% in PAT.

✅ Improving asset quality: Declining NPAs and steady risk-weighted exposure.

✅ Capital buffers strengthened: CAR comfortably above RBI thresholds.

5. Competitive Strengths

6. Key Risks & Challenges

⚠️ Unsecured Lending Risk: Growing share of unsecured loans (personal, micro, education) can raise credit costs in downturns.

⚠️ Valuation Sensitivity: IPO pricing below unlisted market rates may cause discontent among pre-IPO investors.

⚠️ Interest Rate Volatility: Margin pressure possible in a high-rate environment.

⚠️ Competition: Banks and fintechs intensifying pricing and distribution challenges.

⚠️ Market Sentiment Risk: Weak secondary market or geopolitical shocks may impact listing-day sentiment.

7. Valuation Overview

8. Investor Strategy & Insights

9. aiTrendview Sentiment Meter

| Factor | Sentiment | Score |

| Financial Strength | Strong | 93 / 100 |

| Growth Consistency | Robust | 88 / 100 |

| Valuation Comfort | Moderate | 75 / 100 |

| Retail Appeal | High | 84 / 100 |

| Long-Term Outlook | Positive | 91 / 100 |

10. aiTrendview.com View

Overall Rating: ⭐ Accumulate / Long-Term Buy (Risk: Medium)

Editorial Summary:

Tata Capital is a high-quality, systemically important NBFC with consistent profitability, strong capital adequacy, and trusted governance. Supported by Tata Sons’ backing and diversified lending, it offers long-term stability over speculative listing gains.

Why aiTrendview.com Likes It

Allocation Guidance

Post-Listing Triggers to Watch

11. aiTrendview.com Disclosure & Important Notice

About: aiTrendview.com is an independent educational and analytical platform offering AI-curated financial insights for investors and learners.

Purpose: This report is intended solely for training and informational use. It is not a research analyst recommendation, investment advice, or SEBI-registered financial opinion.

Data Sources: Analysis derived from public filings, regulatory documents, and verified financial databases as of October 2025, combined with AI summarization and human editorial review.

Conflicts & Independence: aiTrendview.com and its authors hold no known financial interest or equity position in Tata Capital. No compensation or commission has been received for this article.

Forward-Looking Statements: All projections and expectations are subject to market risk. Past performance does not guarantee future returns.

Investor Caution: Always consult a certified financial advisor before investing. Market conditions and individual suitability must be evaluated independently.

Contact: For corrections, clarifications, or conflict disclosures, contact support@aitrendview.com.

Final Verdict (aiTrendview Summary)

✅ Short-Term: Moderately Positive — steady anchor support and credible fundamentals.

💼 Long-Term: Strong Buy for stability-oriented investors — robust capital, digital transformation, and Tata Group stewardship make this one of the most solid NBFC listings in recent memory.