NSB BPO Solutions Limited is an established IT-BPO and business services company with a diversified service offering that includes back-office processing for telecom, banking & financial institutions, and trading/retail related activities through group entities. Incorporated in 2005 and converted to a public company in 2024, the business has developed long-standing client relationships, an experienced promoter team and a track record of delivery in quality and timeliness. The promoter and driving force behind the business is Narendra Singh Bapna.

2) Industry & Market Context

IT-BPO and business process services remain core outsourced functions for banks, telecoms and enterprise clients. India continues to be a global delivery hub for cost-efficient BPO services; demand dynamics depend on corporate IT spend, digital transformation budgets, and outsourcing decisions by large enterprise clients. For a smaller/sme-listed BPO, winning scale, maintaining pricing, and ensuring data security and uptime are the key competitive levers.

3) IPO Snapshot & Present Status (current offer mechanics)

Offer type: Fresh Issue (100% fresh)

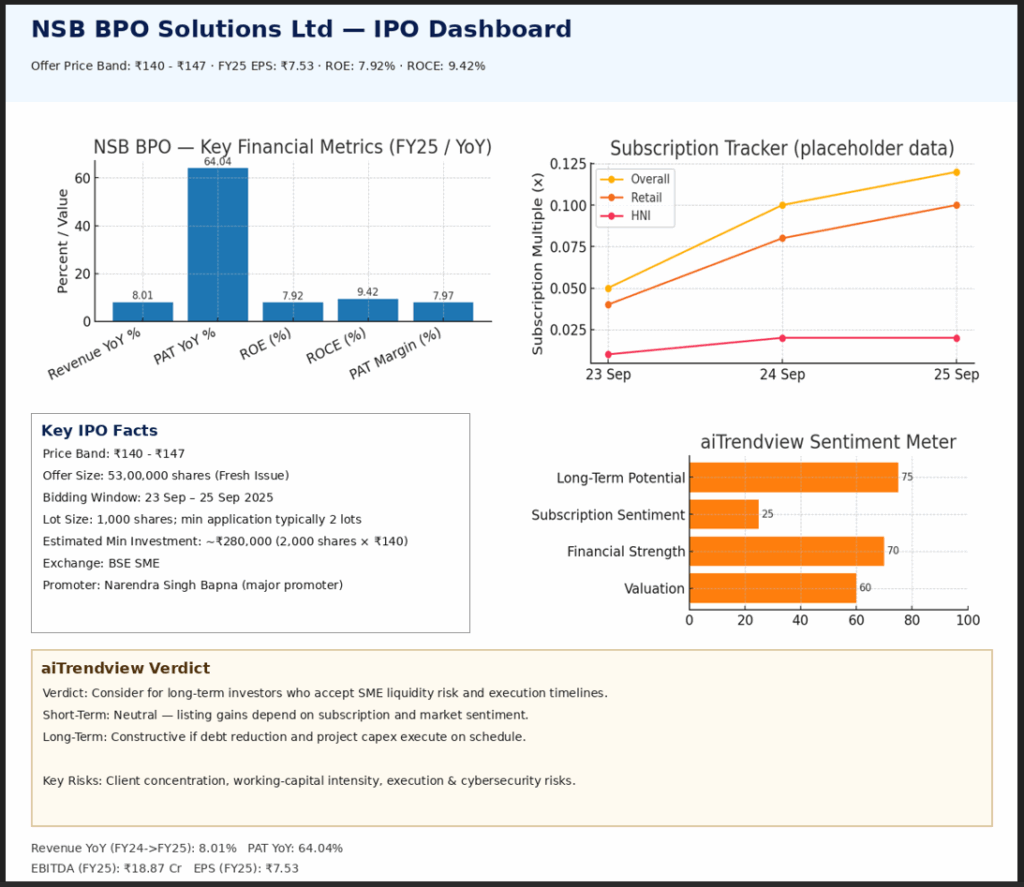

Offer size:53,00,000 equity shares (face value ₹10 each) — total amount to be finalised at the offer price.

Market maker reservation: 2,65,000 equity shares reserved for the market maker.

Price band (announced):₹140 (Floor) — ₹147 (Cap) per share.

Bid / Issue period:Open: 23 Sep 2025 — Closes: 25 Sep 2025 (check the final prospectus/advert for any changes).

Minimum application / lot: Trading lot 1,000 shares. Minimum application is typically 2 lots (2,000 shares) — the minimum application amount will therefore be above ₹2 lakh depending on final price.

Designated exchange: SME platform of BSE (proposed listing).

Current status: Price band set; book-building window scheduled. Subscription progress during the bid days will determine allotment and short-term listing dynamics.

FY25 shows strong improvement in margins and profitability versus FY24 — EBITDA margin moved to ~13.6% and PAT to ~8%.

EBITDA grew markedly in FY25 while revenue rose modestly from FY24 — implying operating leverage and cost control.

FY23 numbers are not directly comparable (FY23 included a large consolidated subsidiary that later became an associate); the restated FY24–FY25 series gives a clearer view of the company’s current operating trajectory.

Cash flow and working-capital dynamics should be reviewed closely (see risks).

PAT: Up ~64% YoY, reflecting stronger bottom-line conversion.

Return ratios: Improving ROCE and ROE but still modest compared with some high-margin software peers — reasonable for a BPO that is scaling.

EPS: Reported diluted EPS for FY25 is ₹7.53.

6) Use of IPO Proceeds (planned allocation)

Proceeds from the fresh issue are intended to be used for:

Repayment / pre-payment of certain borrowings (largest allocation).

Capital expenditure for a new project (capacity / infrastructure).

Additional working capital for existing business operations.

Long-term working capital for the new project.

General corporate purposes (subject to a capped limit).

The company has provided itemised rupee allocations (to be finalised once offer price is determined), and intends to complete deployment during FY2026 (subject to finalisation and monitoring).

7) Key Financial Ratios (FY25 snapshot)

Revenue: ₹138.54 Cr (Total income)

EBITDA margin: 13.62%

PAT margin: 7.97%

EPS (diluted FY25): ₹7.53

ROE: 7.92%

ROCE: 9.42%

Net debt / Borrowings (as of Aug 31, 2025): Outstanding indebtedness ~₹30.11 Cr (company proposes to repay part of this from IPO proceeds)

Valuation at price band (quick math)

P/E (based on FY25 EPS 7.53): At ₹140 → 18.6x | At ₹147 → 19.5x

Using weighted average EPS metric, implied P/Es rise into low-20s.

Compared to high-growth tech peers, these P/Es are moderate — but industry peers’ P/Es vary widely. Use these P/Es in conjunction with cash-flow and growth outlook.

8) Competitive Strengths (what works in NSB’s favour)

Operational history & delivery quality — long-standing presence in BPO services with strong service-level focus.

Improving margins & profitability — operating leverage starting to reflect in FY25 results.

Planned debt reduction via IPO proceeds — strengthens balance sheet and reduces interest burden.

Diversified group ecosystem with retail/trading and other group entities that can provide cross-sell/scale advantages.

Experienced promoter with an entrepreneurship track record and previous SME listing experience in group companies.

9) Risks & What to Watch

Client mix concentration: A large portion of revenue comes from IT-BPO services — any loss/downsizing by large clients can materially hurt revenue and cash flows.

Working-capital & cash-flow: The company plans to use IPO proceeds to reduce debt and fund working capital — past cash flows showed stress and working-capital intensity remains a focus area.

Execution risk for capex/new project: The company proposes capex and a new project which will require timely execution to generate expected returns.

Technology/cyber/security risks: BPO operators hold sensitive customer information — breaches or service outages can affect reputation and client contracts.

SME-listing liquidity / subscription risk: SME IPOs can show muted listing performance if subscription is weak; short-term listing gains are not guaranteed.

Promoter dependence: Business relies on promoter leadership; any disruption here could affect operations.

10) Peer / Valuation Context (directional)

Using FY25 EPS (₹7.53), the P/E at ₹140–147 sits in the ~18.6–19.5x range. On weighted EPS basis the P/E moves into the low-20s.

Industry listed peers have a wide P/E dispersion — some higher-growth or larger players trade at materially higher multiples, while traditional service providers trade at lower multiples. This IPO’s valuation is moderate relative to high-growth software names but needs to be balanced with FY25 margin improvement and the company’s realistic cash-flow outlook.

11) Who should apply & practical requirements to buy the IPO

Who this IPO may suit

Investors wanting exposure to organised BPO / services with improving profitability and an appetite for SME/liquidity risk.

Long-term investors willing to hold through post-listing illiquidity and execution phases.

Checklist & requirements to apply

Active Demat account (NSDL/CDSL) and linked bank account.

KYC / PAN / Aadhaar documents up-to-date.

Apply via ASBA (Applications Supported by Blocked Amount) through your bank or broker’s IPO portal, or via UPI-based ASBA (if available).

Know the lot & minimum application: Trading lot 1,000 shares; minimum application often 2 lots (2,000 shares) — confirm the public announcement and compute the minimum amount (2,000 × Offer Price).

Fill bid carefully: For book-building, place bids within the price band; for fixed offerings follow the exact instructions in the broker/netbanking form.

ASBA block: Ensure sufficient funds are available; funds will be blocked (not debited) until allotment.

After allotment: check allocation status, confirm final debit and allotment credit to your demat.

12) aiTrendview Verdict — Short summary & recommendation

Short-term listing outlook:Neutral / Cautious. SME listings depend heavily on subscription and market sentiment; expect limited liquidity early. Medium- to long-term outlook:Constructive if management executes on debt reduction, converts margin expansion to stable cash flow, and the new project ramps without major delay. Valuation view: At ₹140–147, the asking multiple is reasonable to moderate against FY25 profitability improvements (P/E ~18–20 on reported EPS). The IPO becomes more attractive for long-horizon investors if you accept SME liquidity risk and are confident in the company’s cash-flow recovery plan. Recommendation:Watch the bidding days for subscription trend, confirm minimum application amount and allotment risk. If you’re a long-term investor comfortable with SME liquidity and execution risk, a measured allocation is reasonable; otherwise adopt a wait-and-see approach and consider buying post-listing if fundamentals hold and liquidity improves.

13) Quick Investor Checklist (before you hit submit)

Confirm final offer price and compute P/E using EPS ₹7.53.

Monitor subscription progress during the bid window — low subscription can reduce allotment chances but can also mean good listing pops if demand surges later.

Review proposed use of proceeds (debt repayment + capex + working capital) and management commentary on timing/milestones.

Evaluate client concentration and ask: how diversified are top clients and contract tenures?

Use of proceeds: Debt repayment, capex, working capital, general corporate.

Verdict:Watch & consider for long-term if you accept SME/listing illiquidity and believe in margin & cash flow improvement. Short-term listing gains are uncertain.

15) Disclaimer

This write-up is an informational summary prepared for investors and does not constitute investment advice, a recommendation to buy or sell securities, or a substitute for detailed due diligence. Check the final prospectus/offer document and consult with a SEBI-registered investment advisor or financial professional before making investment decisions. Market conditions and the final offer price/allotment outcomes will materially impact post-listing performance.